PANTRY DELOADING

During the first several weeks of the COVID-19 pandemic, pantry staples like pasta, rice, beans and canned tomatoes were hard to find. Consumers turned to secondary brands just to stock up and shelves were emptied around the nation. It seems like half of the posts on Facebook were about items we could (or couldn’t) find at the grocery store.

In spite of this massive spike in sales, many CPG brands pulled back on their advertising. There were too many unknowns in the supply chain, not to mention consumer sensitivity and economic concerns. Although CPG spending and shopping habits are settling into a new normal, questions still remain.

One question we hear over and over is: were those pandemic-related sales sustainable? Which leads to: Will any of those new shoppers keep buying my brand now that their first choice is available? Will we see a drastic drop in sales as consumers work through the stock in their pantries?

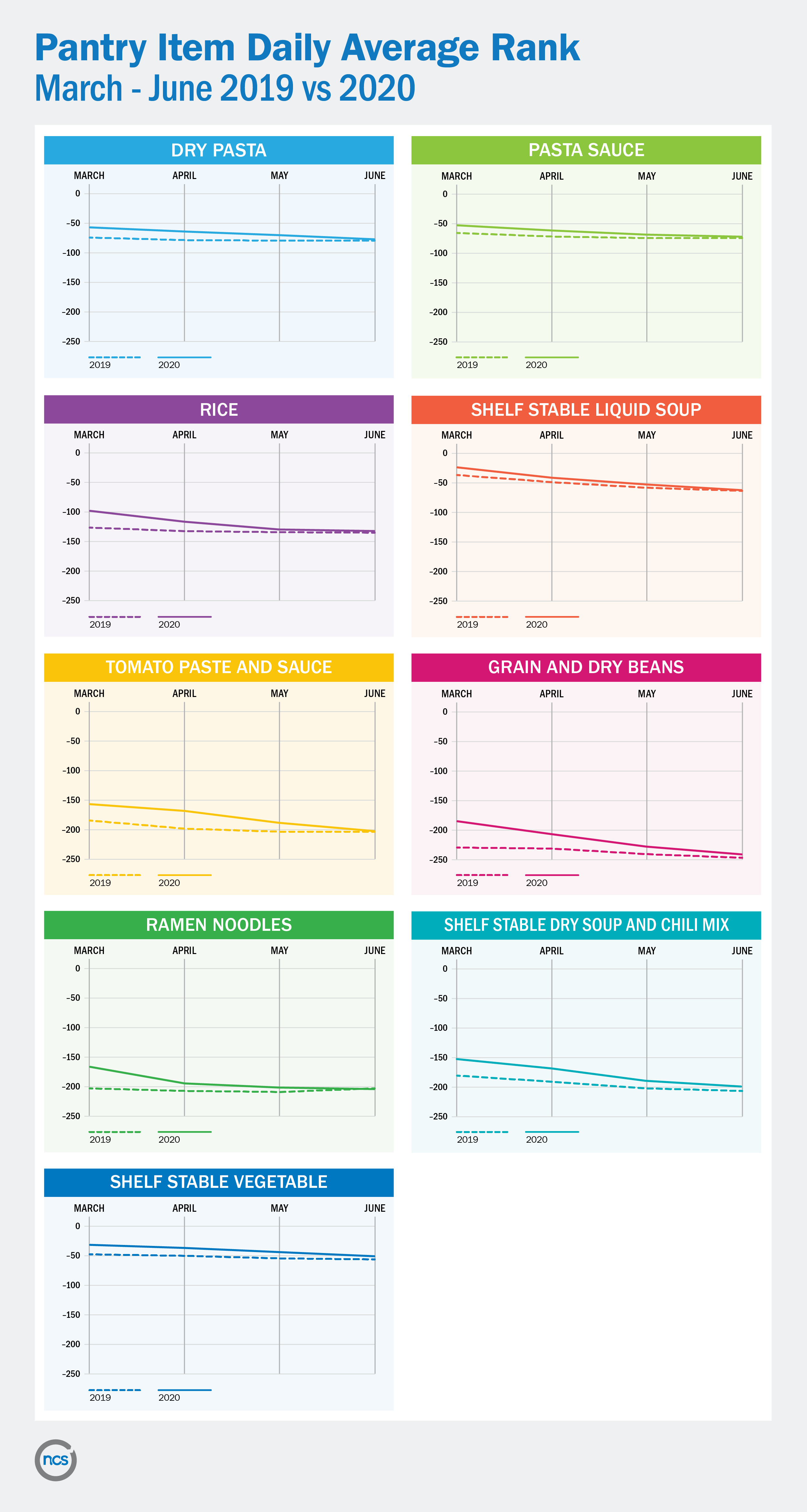

To help guide CPG advertisers on the path forward, we turned to the numbers. According to analysis of shopping data from over 51 million U.S. households, purchasing of pantry staples in June 2019 looks…a whole lot like it did in 2020.

But what does this mean?

According to sharp declines in category rank, the U.S. is experiencing the effects of pantry deloading on staples that were purchased in extreme quantities during March and April. While all of the items we looked at do experience a seasonal decrease in the summer, the drops this year are much more pronounced (though by the end of June they netted out at rankings comparable to last year’s).

As consumers work through their pantry stock, CPG advertisers still have the opportunity to turn new triers into loyal buyers. Perhaps, by advertising to shoppers who hadn’t purchased the product at all in 2019 but tried it in March or April of this year, your brand may win a new buyer for life.