OUT WITH THE OLD?

While the past 10 months have signaled a unique moment in time, brands have had the opportunity to set new priorities and reevaluate what’s working.

Over the last year, the tone of ad content has become even more critical in creative development. Advertisers have had to learn to be extremely agile, creating content that can be adapted or changed as sentiment swings with national events. And many priorities have shifted. Whether for the short term — or for good — only time will tell.

The Big Game is one example of how things look different for CPG brands in 2021. As other priorities have emerged, many brands have decided to reallocate the large budgets that were historically spent on advertising during the big game into other programs or channels.

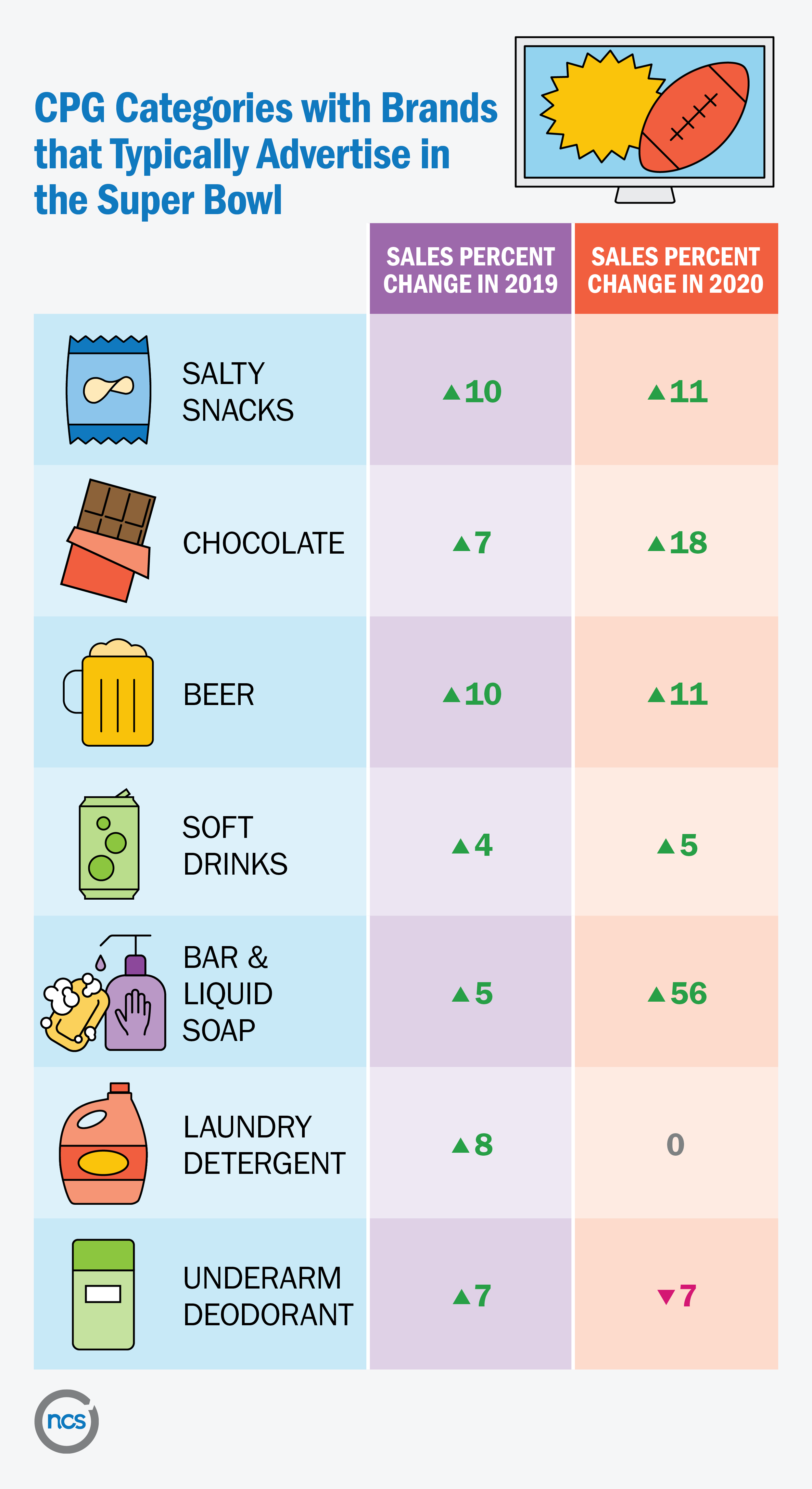

While there are salty snack, soft drink, chocolate and beer brands still planning to advertise in the game this year, brands in many other categories that typically show up have not taken the plunge. Personal care brands in the soap and deodorant subcategories are on the list of those that we typically see advertising during the Big Game, but don’t seem to be on the docket for 2021.

To understand what factors may be driving these decisions, we took a look at sales growth in these categories. With the exception of laundry detergent, the categories that we again see advertising in the Big Game had a relatively stable year. In terms of growth, 2020 didn’t look a whole lot different than 2019. Perhaps a little more stability and predictability is what gives advertisers the confidence they need to make large commitments.

As the year progresses, we’ll continue to watch the trends to see how the pandemic is impacting CPG shopping behavior.